AI for Credit Unions

Governance, fraud, vendor risk, lending, contact center, operations, and member-experience coverage in one editorial guide.

Explore the hub →

CreditUnionAI News

Coverage of artificial intelligence regulation, fraud, vendor risk, lending, operations, and member experience for credit unions.

Start with durable coverage areas that credit union leaders search for: AI strategy, vendor risk, governance, fraud, lending, and operations.

Governance, fraud, vendor risk, lending, contact center, operations, and member-experience coverage in one editorial guide.

Explore the hub →Due diligence, contracts, hidden AI features, agent permissions, audit evidence, and board oversight for third-party AI systems.

Explore vendor risk →Get weekly AI alerts and analysis written for credit union boards, executives, risk teams, and operators.

Subscribe →Curated headlines on AI regulation, vendor moves, and frontline member experience.

Board directors and supervisory committee members must ensure that AI-driven knowledge retrieval and policy copilots for elder fraud, caregiver permissions, and vulnerable-member protection produce auditable evidence. Without rigorous complaint evidence trails, credit unions risk examiner findings and member harm.

Credit union vendor management officers face new AI agent governance requirements. Learn how to set permissions, approval queues, and action limits for vendor procurement and contract renewals without creating audit gaps or member-impact failures.

Credit union CIOs must pair deepfake detection with operational artifacts—board memos, risk registers, call transcripts—to avoid audit gaps and member harm.

Credit unions deploying embedded finance and open banking APIs face the insights-impact gap: behavioral data flows but prescriptive actions stall. practical steps for loan underwriters to bridge that gap using vendor contracts, risk registers, and board memos.

As credit unions adopt FedNow, RTP, and tokenized cash under the GENIUS Act, loan underwriters face the insights-impact gap: legacy core silos block real-time prescriptive insights. Data fabric, zero-migration layers, and open core mesh architectures offer a path forward, but operational discipline is critical to avoid audit gaps, frontline confusion, and member-impact failures.

Frontline branch staff and MSRs are caught in the core modernization dilemma: evaluating zero-migration data fabrics versus costly wholesale legacy core replacements. This article explores how data fabric, zero-migration layers, and open core mesh architectures can be applied to high-yield deposits and predictive CD retention liquidity, while avoiding audit gaps, frontline confusion, model-risk blind spots, and member-impact failures. Practical operational artifacts such as board memos, vendor contracts, risk registers, call transcripts, loan files, case notes, audit evidence, and control reviews are referenced.

As credit unions deploy AI to summarize member calls, compliance leaders must ensure these summaries are monitored for complaints and backed by immutable audit trails. This article examines the operational artifacts—board memos, vendor contracts, risk registers, call transcripts, and QA reviews—needed to build a defensible workflow.

Many credit unions are unaware of AI features already operating within their vendor platforms. This article provides a vendor management and contract review workflow to inventory these hidden AI capabilities, using board memos, vendor contracts, risk registers, call transcripts, loan files, case notes, checklists, audit evidence, and control reviews. The goal is to tighten policies, vendor evidence, fraud defenses, and member-data controls before habits harden.

Voice cloning technology has advanced to the point where a few seconds of audio can be used to impersonate a member. For credit unions, the contact center is ground zero. This article outlines a practical workflow—contact center authentication and step-up verification—that fraud and member service leaders can implement now to close the vulnerability without disrupting the member experience.

AI-agent breakthroughs point to a practical credit union workflow: using AI to help with auto loan hardship intake, missing documents, servicing notes, and human-approved follow-up.

Credit unions do not need a yearlong AI committee before taking action. A 90-day governance calendar can create inventory, policy, vendor review, and pilot discipline fast.

For many credit unions, after-call summaries are a safer first AI contact center pilot than a member-facing chatbot because they improve staff workflow without putting AI between the member and help.

AI features are entering renewals and add-ons. Credit unions need sharper contract questions before vendor AI becomes embedded in member, lending, fraud, or operations workflows.

AI readiness is not one checklist. Each leadership segment needs a different playbook before governed execution can scale.

A staged ladder helps teams start with safer internal workflows before climbing toward sensitive member-facing automation.

Map tool exposure, data exposure, control evidence, and business value before another AI feature becomes operational risk.

Practical rules that protect member data, preserve human judgment, and give teams clear boundaries for employee AI use.

A practical way to evaluate AI vendors before tools become embedded in member, lending, fraud, or operations workflows.

Board-level questions for overseeing AI adoption, vendor risk, data protection, human review, and accountability.

The shift from AI experiments to governed, operational AI is now unavoidable.

Why AI-assisted messaging is emerging as a practical, trust-preserving entry point for credit unions.

Practical applications across fraud, lending, compliance, marketing, and internal productivity.

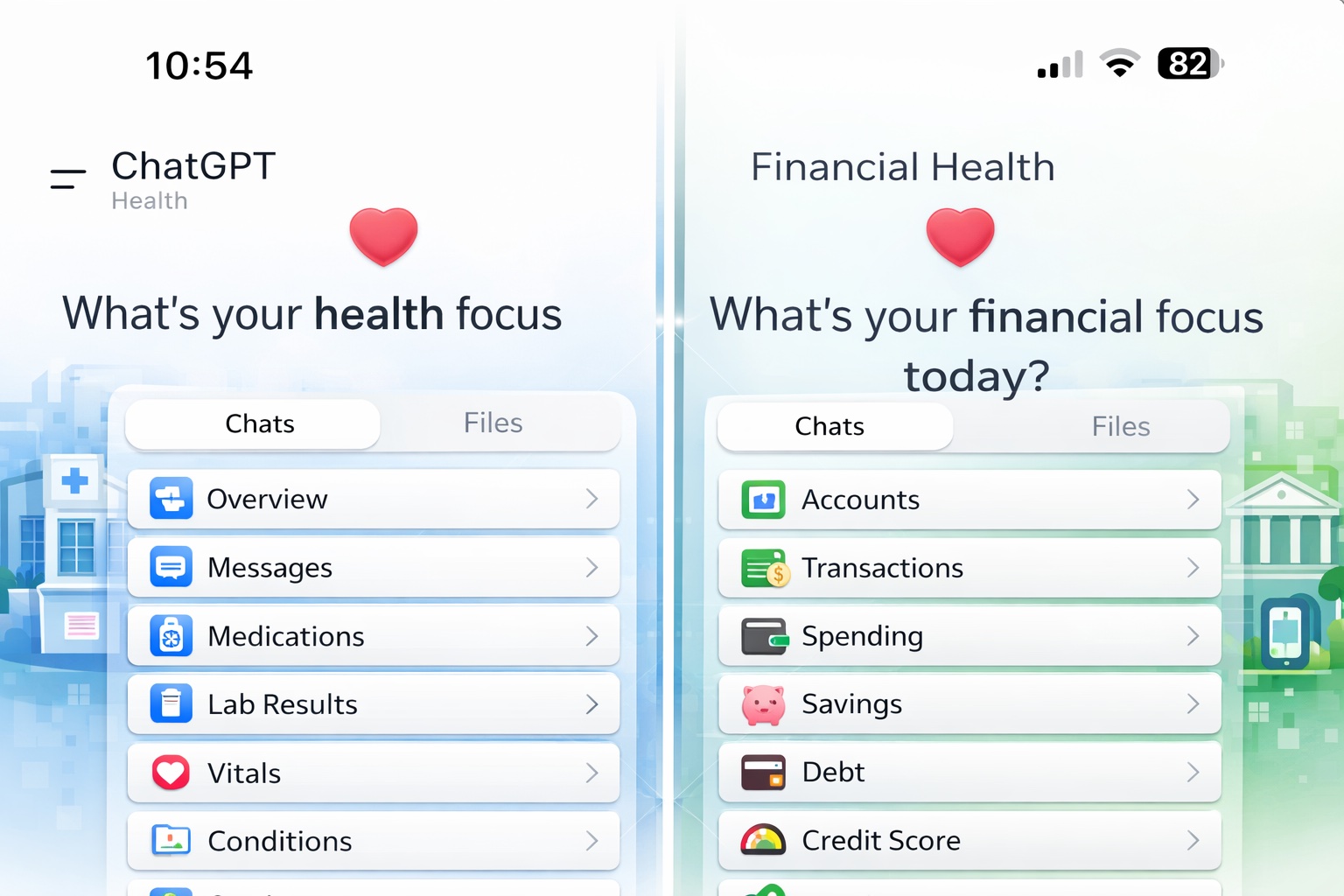

ChatGPT Health previews how AI platforms could become the primary interface for banking and fintech.

Fintech and payments vendors emphasized AI as embedded infrastructure for authentication, fraud prevention, compliance workflows, and transaction decisioning.

Practical benchmarks for AI governance, fraud defenses, employee enablement, and operational gains heading into 2026.

How frontline, operations, lending, and compliance teams can safely benefit from the latest assistant improvements.

Posh framed structured AI Operating Procedures to pair agentic automation with bank-grade controls and auditability.

Invictus Growth Partners’ investment underscores lender demand for AI fraud detection and document verification.

Reuters highlights firms keeping escalation paths in place as AI handles simpler service requests.